یہ بھی دیکھیں

17.02.2026 03:40 PM

17.02.2026 03:40 PM

*) see also: InstaTrade trading indicators for DJIA (INDU)

Futures on the Dow Jones are trading in a local sideways trend around 49,450.0–49,500.0 at the start of the US Tuesday session, having firmed slightly after a sharp drop during the Asian session. US equity indices, including the DJIA, are being supported by macro data on the labor market and inflation that signal a near-term return to a dovish Fed policy cycle. On the other hand, they are under significant pressure from tectonic shifts in the technology sector.

Investors remain in a holding pattern ahead of key releases — the FOMC minutes on Wednesday and the PCE inflation report on Friday.

Current situation: macro support vs. tech storm

US January inflation came in softer than expected: the consumer price index (CPI) slowed to 2.4% year-on-year, the lowest reading since April 2025. Core CPI also eased to 2.5%, the weakest reading since April 2021.

At the same time, the labor market is showing mixed but broadly stable signals. Nonfarm payrolls rose by 130.0k in January, beating expectations and allowing the unemployment rate to adjust to 4.3%. That combination — slowing inflation alongside a resilient labor market — strengthens expectations for a Fed pivot to a dovish stance as soon as June, immediately after the anticipated change in leadership at the central bank in May.

But optimism is tempered by a powerful wave of selling across the technology sector. Fears about the disruptive impact of AI on traditional business models have triggered a large-scale rotation of capital. AI tools such as Anthropic's Claude Cowork have raised concerns about structural pressure on conventional software business models.

Capital rotation: Dow Jones looks more resilient than Nasdaq

Despite broad volatility, the Dow Jones is showing relative resilience compared with technology indexes. While the Nasdaq Composite (or the NASDAQ100 — NDX in the trading terminal) recorded its fifth straight weekly decline (the first such sequence since 2002), the Dow fell only 1.2% last week. The reason is a structural rotation of capital out of overheated tech names into formerly undervalued sectors.

Since the end of 2025, a clear trend has emerged: investors are leaving large technology stocks and shifting into sectors that did not participate in the AI rally. Among the beneficiaries of this rotation are:

Unlike the S&P 500, the Dow Jones has a smaller share of technology companies in its composition, making it a natural shelter during technology turbulence. The index is being supported by growth leaders such as Nike (+3.32%), UnitedHealth Group (+3.10%), and Walt Disney (+3.00%). At the same time, tech components in the index — Apple (-2.27%) and Visa (-3.12%) — are weighing on the level.

Fed factor: leadership change and policy shift

A key driver of medium-term expectations remains the forthcoming change of leadership at the Federal Reserve. In late January, President Trump nominated Kevin Warsh to replace Jerome Powell, whose term expires in May. Warsh, a Wall Street veteran and former Fed governor, is known as a critic of current policy. He advocates substantial institutional changes, including shrinking the Fed's balance sheet to withdraw excess liquidity, which he believes would create conditions for further lowering borrowing costs.

Markets have interpreted the nomination as a signal of potentially more dovish policy, despite concerns about central-bank independence.

According to the CME Group's FedWatch tool, investors currently assign roughly an 8% probability to a 25-bps cut in March and a 53% probability to a cut in June.

Corporate sector: mixed signals

The active earnings season has concluded, but individual results continue to shape sentiment. Semiconductor-materials maker Applied Materials Inc. reported revenue of $7.01 billion, beating expectations ($6.87 billion) but below last year's result ($7.17 billion). Earnings per share came in at $2.38, matching last year's figure.

This week, investors will watch reports from Walmart, Warner Bros. Discovery, and Booking Holdings, which could offer additional insight into the consumer sector and corporate spending.

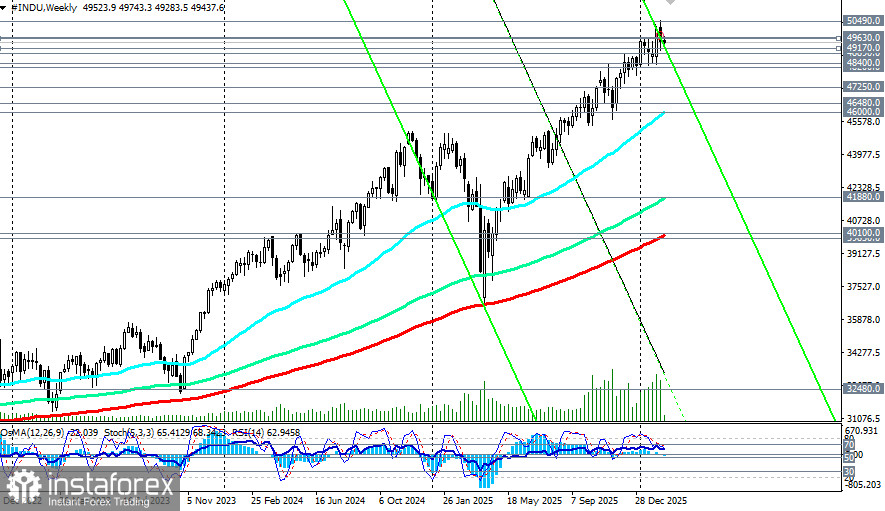

Technical picture

Technically, futures on the Dow Jones (or DJIA — INDU in the trading platform) remain in an uptrend, although momentum is slowing. Indicators (RSI, OsMA, Stochastic) on the daily chart have turned bearish. Key support is in the 49,000.0–48,890.0 zone (EMA50 and the lower line of the rising channel on the daily chart); a break below that area could open the door to a deeper correction. Immediate resistance lies around 49,630.0 (EMA200 on the 1-hour chart) – 497,500.0 (local highs).

*) for more detail see DJIA (INDU): scenarios of dynamics on 17.02.2026

Conclusion

The Dow Jones currently acts as a kind of safe haven in the turbulent sea of the US equity market. Structural capital rotation from overheated tech names into defensive and cyclical sectors creates a constructive backdrop for the index. At the same time, macro signals — slowing inflation and a stable labor market — increase expectations of near-term Fed easing, which is traditionally positive for equities.

The key risk remains an escalation of panic around artificial intelligence and its impact on traditional business models. However, given the Dow's lower reliance on the technology sector and solid macro indicators, the index has every chance of holding within current ranges and even resuming gains after the Fed policy picture clears. Investors' attention this week will be on the FOMC minutes on Wednesday and PCE inflation data on Friday, which could become catalysts for the next significant move.