Vea también

18.02.2026 09:57 AM

18.02.2026 09:57 AMWhen everyone is selling, it is a great chance to buy cheaper. The market is slowly moving on from the tech-led rout. After Presidents' Day, the S&P 500 opened with a gap down, with the Magnificent Seven stocks falling to their lowest levels since September. Still, upbeat news from NVIDIA, which expanded its chip and equipment supply to Meta Platforms, helped the group finish the day in the green.

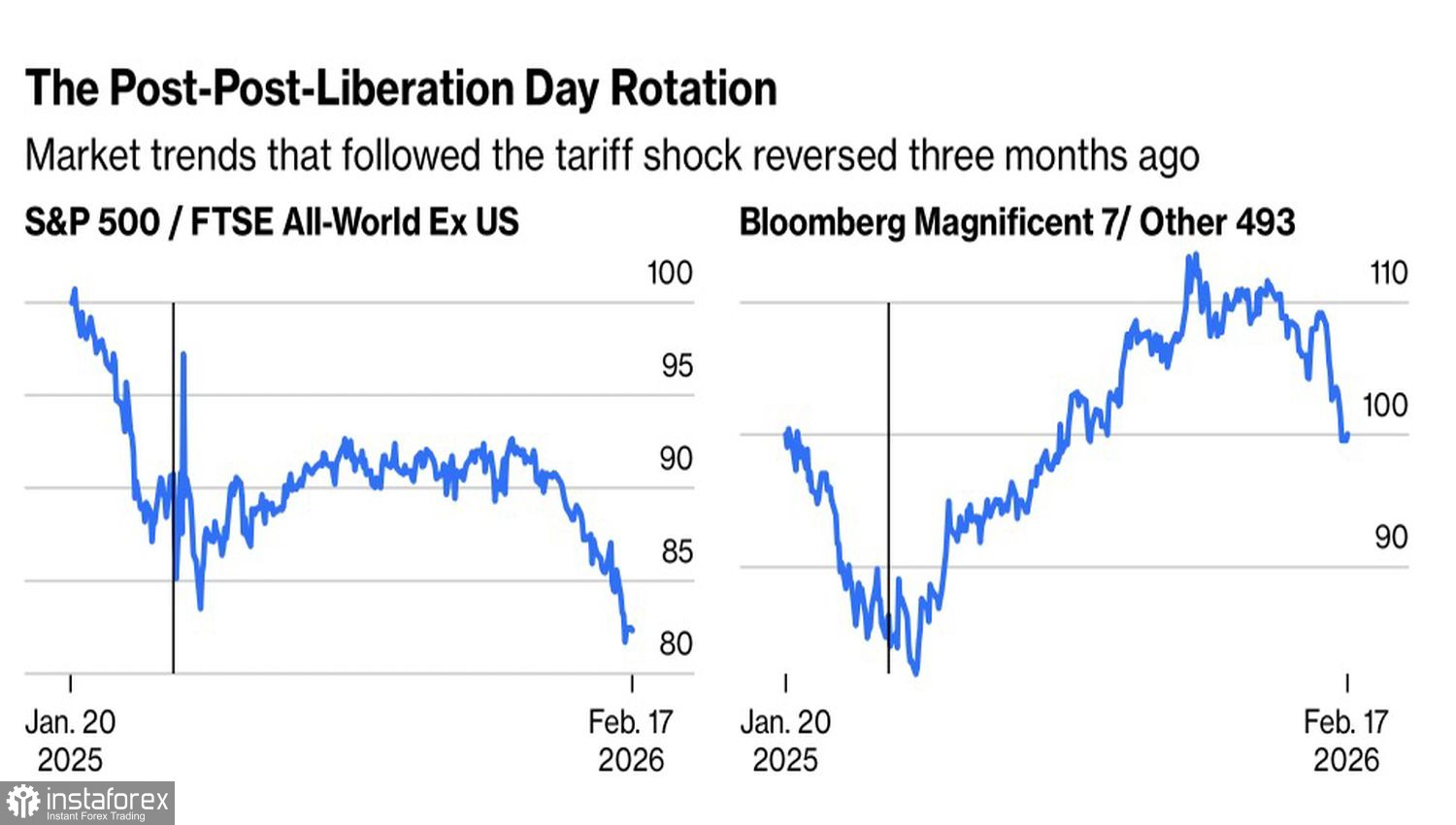

The main driver of the February pullback in the S&P 500 is not a weak US economy or disappointing corporate results; it is plain rotation. Investors are debating which firms will lose most from artificial intelligence and are actively getting rid of yesterday's winners, the mega cap tech stocks. As a result, the ratio of the Magnificent Seven to the other 493 S&P 500 issuers is sliding.

Dynamics of S&P 500 relative to global stock index and G7 relative to other companies

The same dynamic is playing out when you compare the broad US index with its global peers. Investors are trimming US equities and parking capital in other regions, Europe and Asia, driven both by uncertainty around Washington's policy and a move away from Big Tech.

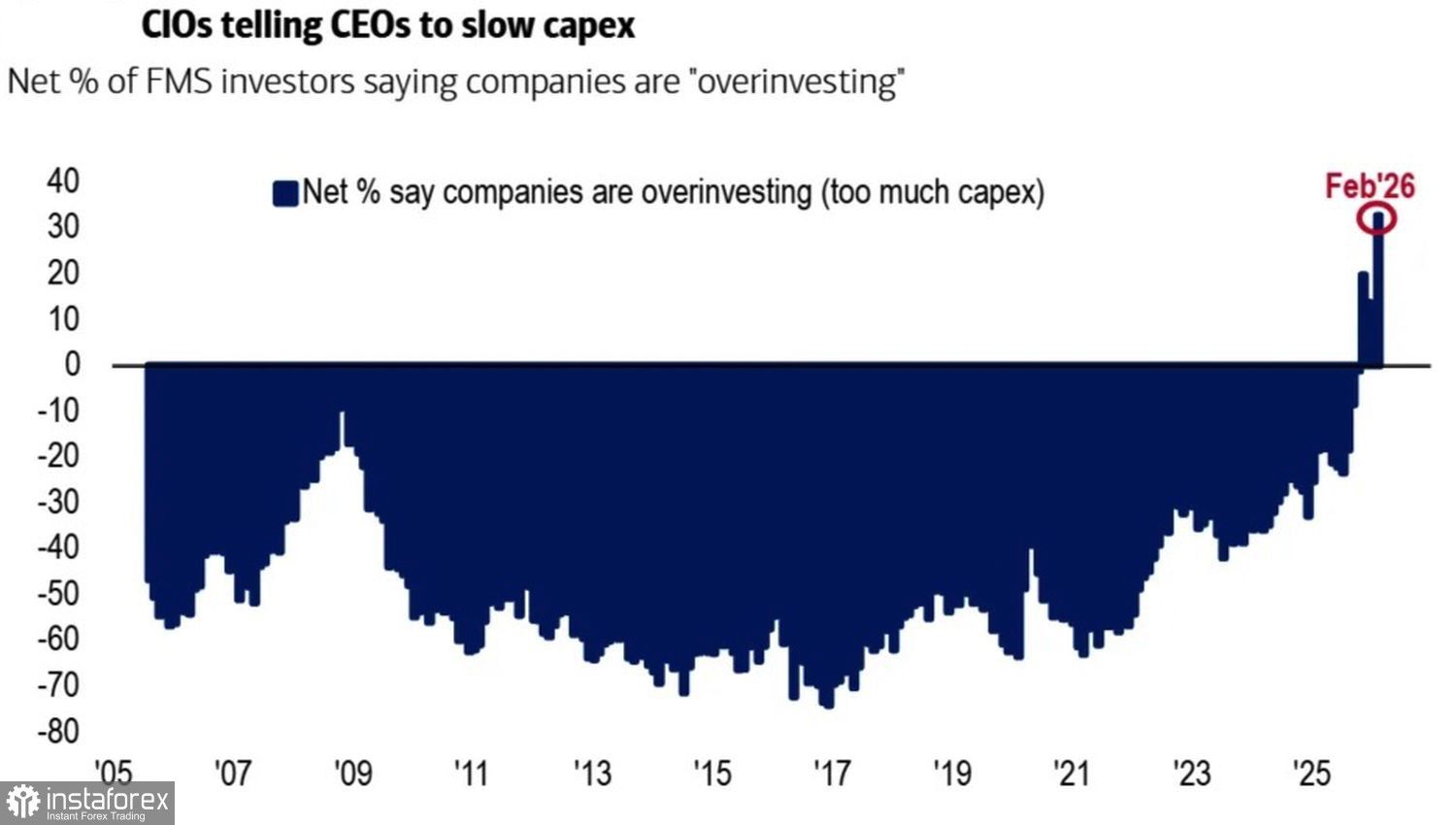

Tech giants are suffering both from stretched fundamental valuations and from the sheer scale of recent investment. Asset managers worry that these massive investments will not generate adequate returns. One of their biggest fears, according to a Bank of America survey, is overinvestment. For decades, fund managers complained about a lack of investment opportunities. Today, however, they are concerned about an excess.

Dynamics of risks associated with underinvestment and overinvestment

On the face of it, you cannot have too much money. However, when capital drains away like water through a sieve, it is hardly comforting. Until AI investments start to show real efficiency gains, that fear will not disappear.

Those same asset managers currently assign only a small — about 6% — probability to a hard landing in the US economy. Some even think that the economy could overheat further if Trump's big tax-cut agenda passes. And faster GDP growth does not necessarily mean higher inflation — a view Kevin Warsh put forward and one that San Francisco Fed President Mary Daly started to echo. With no new Fed chair yet in place, it seems that FOMC members are already trying to please him.

Maybe it is time to buy deeply discounted stocks, but no one is eager to catch those falling knives just yet.

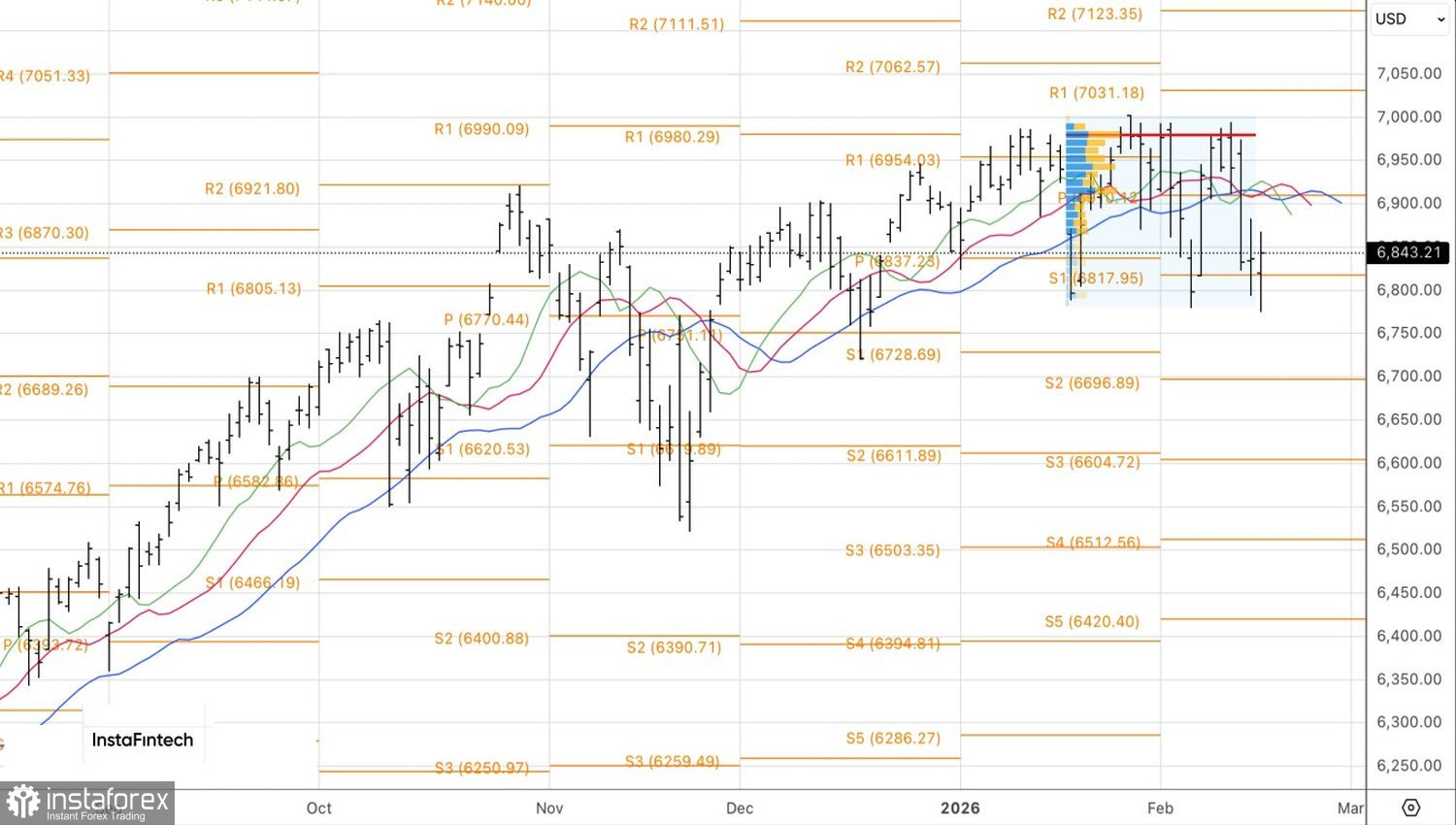

Technically, the S&P 500 daily chart is shaping a potential double bottom pattern. Whether bulls can defend it and return to an uptrend depends on the battle at 6,815. A drop below that level would justify renewed selling. As long as the index trades above it, the bias remains toward buying.