यह भी देखें

10.07.2026 07:30 PM

10.07.2026 07:30 PM

GBP/USD posted a strong rally that may mark the beginning of a broader bullish trend. In my view, the US dollar's appreciation between June 17 and June 24 was not supported by the fundamental backdrop. By that time, the geopolitical conflict in the Middle East had already been halted, even though it had been the primary driver of the dollar's strength throughout 2026. Therefore, it seems inconsistent for the dollar to strengthen first because of the war and then continue strengthening after the conflict had effectively ended.

It is also surprising that the US dollar failed to gain this week despite a fresh escalation in the Middle East that could have serious consequences. Donald Trump announced the end of the ceasefire and revoked the authorization allowing Iran to sell oil under the terms of the peace agreement. As a result, the period of relative calm has come to an end. However, traders have so far remained skeptical that the conflict will resume, as similar situations have occurred several times before, with both sides eventually returning to negotiations. In my opinion, the market's limited reaction to the renewed geopolitical tensions is justified.

It is also worth noting that the market initially expected higher US inflation unless the Federal Open Market Committee (FOMC) intervened. Later, inflation concerns eased as oil prices fell to around $70 per barrel. This week, however, oil prices climbed back toward $80 per barrel, and the latest escalation in the Middle East could once again result in a blockade of the Strait of Hormuz and Iranian ports.

Should events unfold according to the most pessimistic scenario, oil prices could quickly return above $100 per barrel. Under such circumstances, hopes for slowing inflation in either the United States or the Eurozone would likely disappear. As a result, the market would once again need to revise its expectations regarding future monetary policy by both the Federal Reserve and the European Central Bank (ECB).

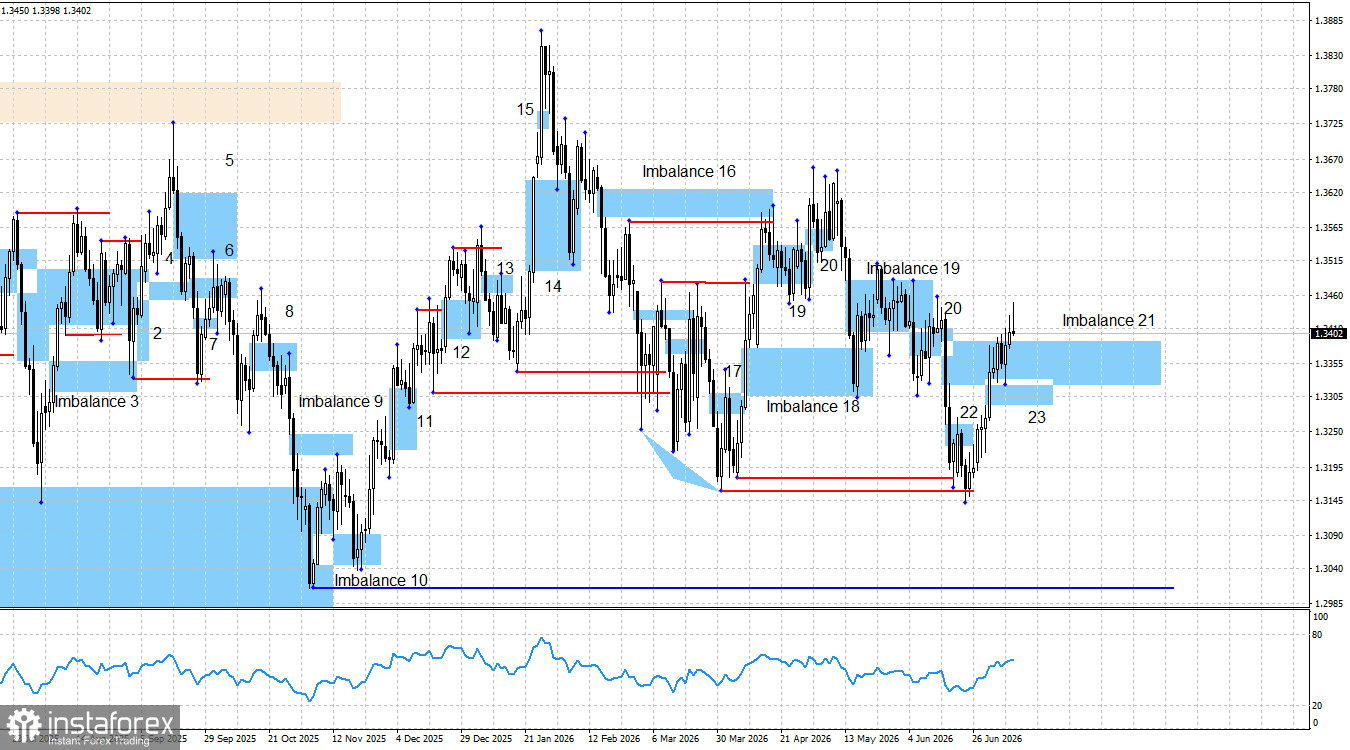

From a technical perspective, the chart suggested a rise toward 1.3322, which is exactly what occurred. The price first swept liquidity below the April 6 low and then below the March 31 low. These liquidity sweeps provided a solid technical basis for expecting further gains in the pound.

Given that the US dollar still lacks convincing long-term bullish drivers—and has already posted an impressive advance during 2026—I believe the bears have largely exhausted their potential. In addition, a bullish imbalance (No. 23) formed last week, and the market has already reacted to it twice.

As for the bearish imbalance (No. 21), I now consider it invalidated. Although the price has not broken through its origin, it has moved too far above the imbalance for it to remain relevant. Therefore, I expect either a continuation of the current rally or the formation of new bullish signals, followed by another upward move after a corrective pullback.

At present, the market remains highly cautious regarding the agreement between Iran and the United States, and recent developments suggest that such caution is justified. Military strikes near the Strait of Hormuz continue to occur regularly despite the memorandum signed several weeks ago.

The Federal Reserve's policy stance triggered a strong rally in the US dollar, yet I still struggle to identify what could allow the bears to maintain further pressure. Can expectations of additional FOMC monetary tightening alone continue to support the dollar?

There were no significant economic releases on Friday. Traders had virtually no macroeconomic data to assess throughout the day. Consequently, technical analysis is likely to remain the primary market driver in the near term.

Overall, the broader fundamental backdrop continues to support a long-term bearish outlook for the US dollar. Neither the conflict between Iran and the United States nor expectations of a Federal Reserve rate hike in 2026 have changed that view.

Geopolitical tensions temporarily reminded investors of the US dollar's traditional safe-haven status, but the conflict has either ended or is at least moving toward a resolution. Although the Federal Reserve intends to raise interest rates in 2026—which is supportive for the dollar—it should also be remembered that tighter monetary policy would likely slow both the US economy and the labor market.

In addition, Donald Trump appointed Kevin Warsh as Chair of the FOMC with the expectation that he would pursue a more accommodative monetary policy—something Trump believed Jerome Powell was unwilling to deliver. For this reason, I do not expect the Fed's tightening to develop into a prolonged tightening cycle. Consequently, I believe any appreciation of the US dollar is likely to be temporary rather than the beginning of a sustained long-term trend.

The economic calendar for July 13 contains no significant releases. Therefore, macroeconomic data is once again unlikely to influence market sentiment on Monday.

The long-term outlook for the pound remains bullish. Following the liquidity sweeps below the two most recent swing lows, buyers have an opportunity to regain control of the market.

The pound could still resume its decline toward 1.3007, the level that would invalidate the bullish trend, but this would require fresh bearish technical signals. Since Bearish Imbalance No. 21 has been invalidated, there are currently no remaining bearish signals from that structure.

The bullish case is supported by the two liquidity sweeps as well as Bullish Imbalance No. 23. The market has already reacted to that imbalance, and the next upward targets are the highs of May 1 (1.3656) and January 27 (1.3867).