यह भी देखें

27.05.2026 01:42 AM

27.05.2026 01:42 AMIn April, the year-on-year inflation rate for consumer prices in the UK decreased from 3.3% to 2.8%. At first glance, this outcome may seem surprising; however, it can be explained by what are known as "base effects." A year ago, in April, inflation surged by 1.25%, and excluding this spike from the annual calculation led to the observed decrease.

Nevertheless, the monthly price increase was 0.75%, which on an annual basis is equivalent to 9%. Prior to the outbreak of the Gulf conflict, these figures had already been accounted for, and a slowdown in inflation to 2% was anticipated.

Even in the event of a swift peace agreement, the inflationary shock is likely to persist for several months. If the conflict drags on and the Strait of Hormuz remains closed, the cumulative effects could last until 2027. This will have a significant impact on production volumes, employment, and, of course, inflation.

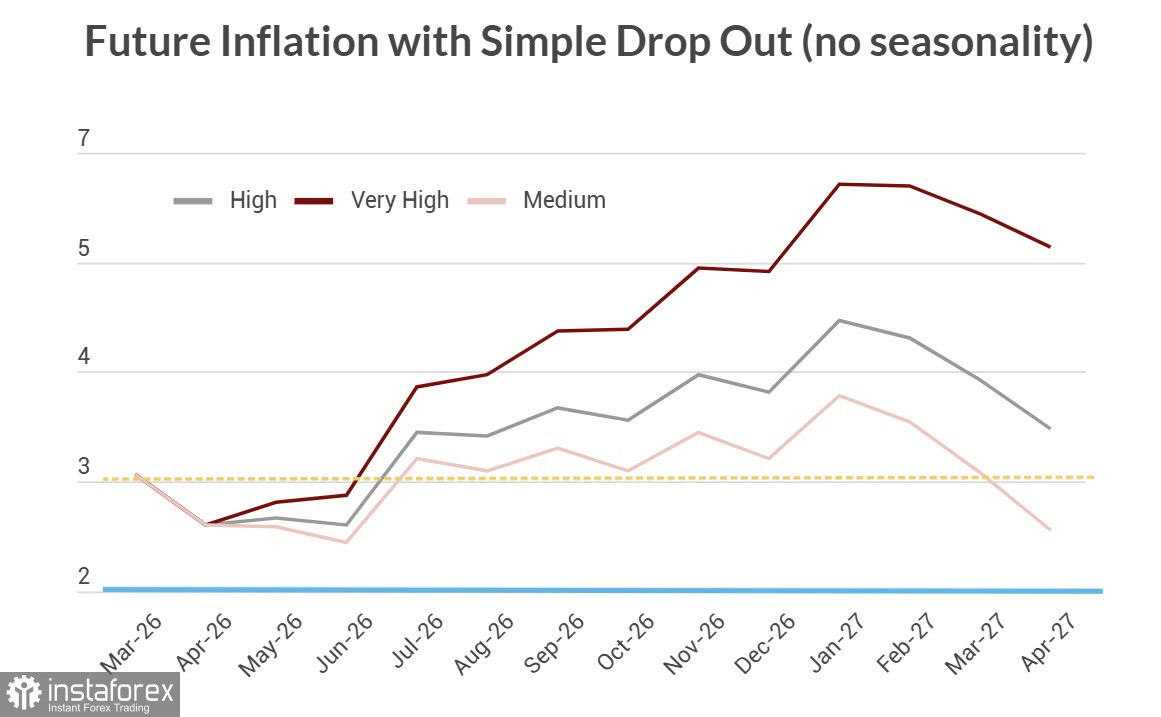

It is forecast that inflation will firmly remain above 3% in the second half of 2026. In such conditions, the Bank of England will not be able to lower interest rates this year. Moreover, as inflation rises towards the end of the year, the central bank will face pressure to tighten monetary policy.

The NIESR Institute offers three scenarios for future price dynamics, ranging from pessimistic to optimistic, yet in all scenarios, inflation will rise throughout the second half of the year, as the main delays in energy supplies began only in May, and even if the Strait of Hormuz is reopened, it will take at least six months for the situation to normalize.

In this situation, the economy's resilience is particularly important, and the latest data appears quite alarming. Retail price growth in the UK slowed in May amid declining demand; prices increased at their slowest pace in over a year, and this pace is expected to continue in June. The Services PMI index, which contributes the most to GDP calculation, sharply slowed in May from 52.7 to 47.9, and the composite index has fallen into contraction territory despite the current resilience of the manufacturing sector.

While the pound appears relatively strong due to a decrease in domestic political risks and is awaiting the release of the core PCE inflation report in the U.S.—which the Federal Reserve is relying on to assess core price pressures—the report will almost certainly lead to a reassessment of the Fed's rate forecasts, most likely in favor of a higher rate, supporting the dollar.

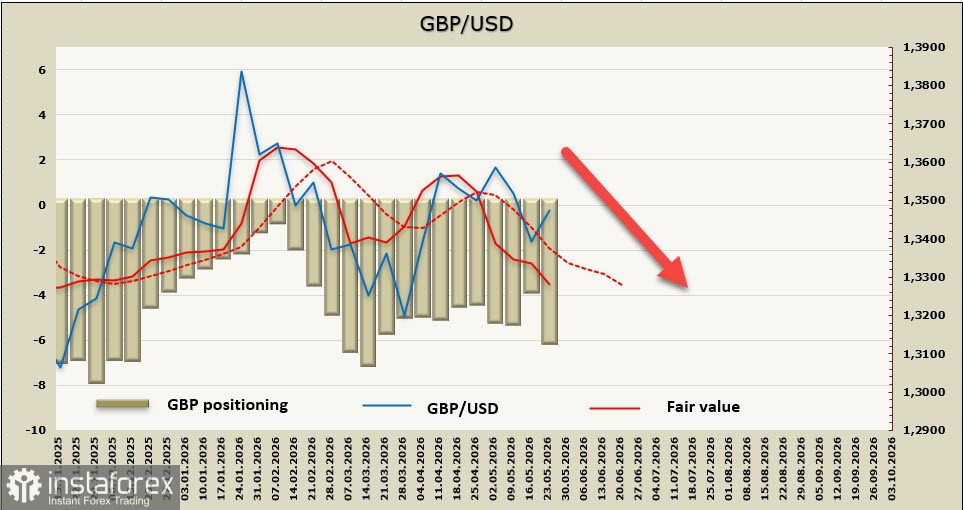

Speculative positioning on the GBP for the reporting week has become even more bearish, with the calculated price steadily declining.

Last week, we prioritized the scenario of further declines in the GBP/USD pair, and this forecast remains relevant. We consider the rebound from the lows to be corrective. We do not expect significant movements until Thursday, as the publication of the PCE may significantly increase volatility. The potential growth of GBP/USD is limited by the resistance zone at 1.3660/80, and we consider a resumption of the decline towards the recent low at 1.3299 to be the more likely scenario.