यह भी देखें

01.04.2026 01:18 PM

01.04.2026 01:18 PM

See also: InstaTrade trading indicators for GBP/USD

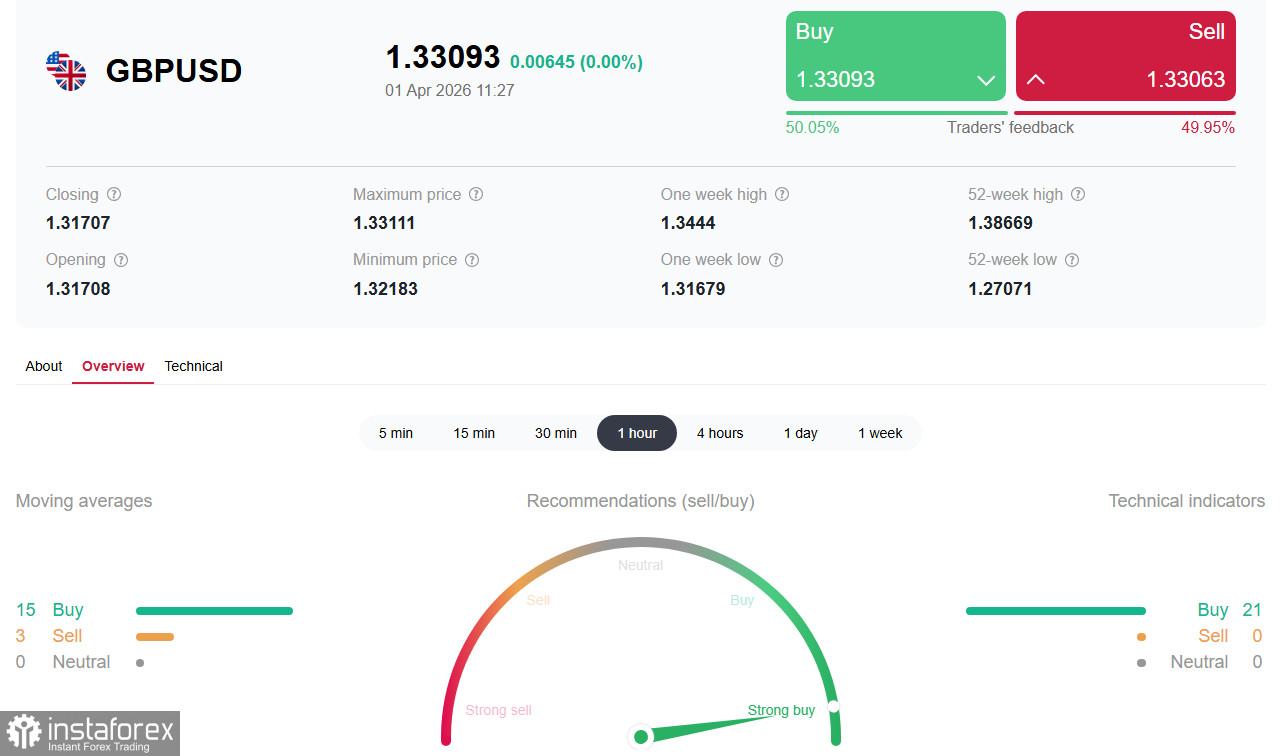

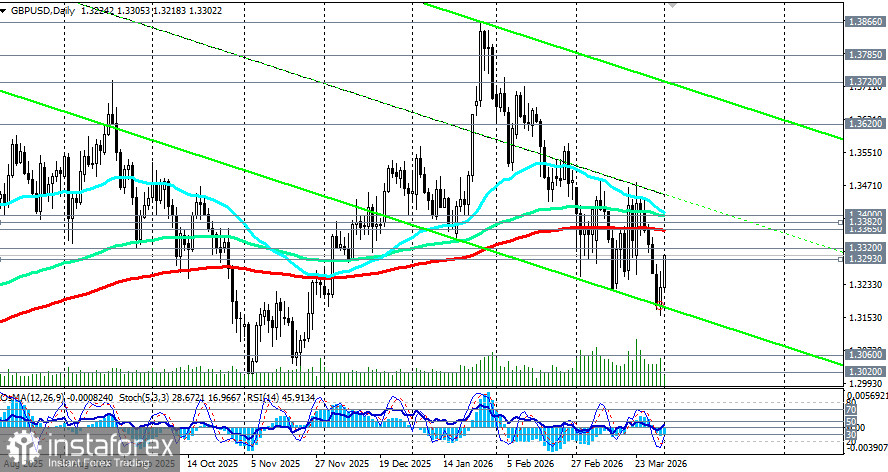

The GBP/USD pair begins the new month with a confident rise, climbing to around 1.3300 — a new weekly high — after a series of positive signals about a possible de-escalation of the Middle East conflict. The pound has found itself at the epicenter of a clash between two forces: on one side, rising hopes for peace that weaken the dollar as a safe-haven asset, and on the other, persistent fundamental weakness in the British economy and uncertainty over monetary policy.

Current situation: hopes for peace and UK GDP data

1. On Tuesday, US President Donald Trump indicated that the US could finish the military operation against Iran within two to three weeks, which sparked optimism about de-escalation in the Middle East. On Wednesday, Iranian President Masoud Pezeshkian said that his country was ready to end the war with the US but demanded certain guarantees to prevent a repeat of aggression.

These statements weakened the US dollar as a safe haven and supported the rise in GBP/USD. The pair bounced off the 1.3160 area (a four-month low) and gained positive momentum for the second day in a row.

2. Yesterday, UK gross domestic product data for the fourth quarter were published and met forecasts: quarter-on-quarter growth accelerated by 0.1%, and year-on-year growth was 1.0%, slightly below the previous period's 1.2%.

Economists note that overall growth at the end of last year remained rather weak, and this was before negative effects from the Middle East crisis. Going forward, the situation may only worsen, which calls into question the need for a hawkish stance from the Bank of England.

Market participants currently have mixed views on the Bank of England's next moves. Some expect two or three rate changes, while most economists believe officials will continue to adopt a wait-and-see stance.

Weak GDP growth in Q4 and the expected deterioration under the influence of the Middle East crisis reduce the need for a hawkish approach.

Key factor: hopes for peace and USD's reaction

Signals of a possible end to the conflict are coming from both sides. US Secretary of Defense Pete Hegseth said recently that the door for a deal is open, and the coming days could be decisive. Iran, for its part, expressed readiness to end the war, demanding guarantees.

As reported by the media, President Trump allows for the possibility of ending hostilities even if shipping restrictions in the Strait of Hormuz remain in place. This stance directly affects global markets: the anticipation of stabilized oil supplies reduces the short-term geopolitical risk premium, which is already reflected in oil prices and rising equity indices.

Yesterday, Federal Reserve Chair Jerome Powell stated that inflation expectations in the country remain stable so far, despite rising energy prices, and therefore the regulator would not react by changing borrowing costs. This remark supported risk appetite and weakened the dollar.

However, economists warn that optimism around Powell, who steps down in May, may be excessive. Gasoline prices in the US rose by 30% over the last month, and Chinese manufacturers are raising export prices by as much as 20%.

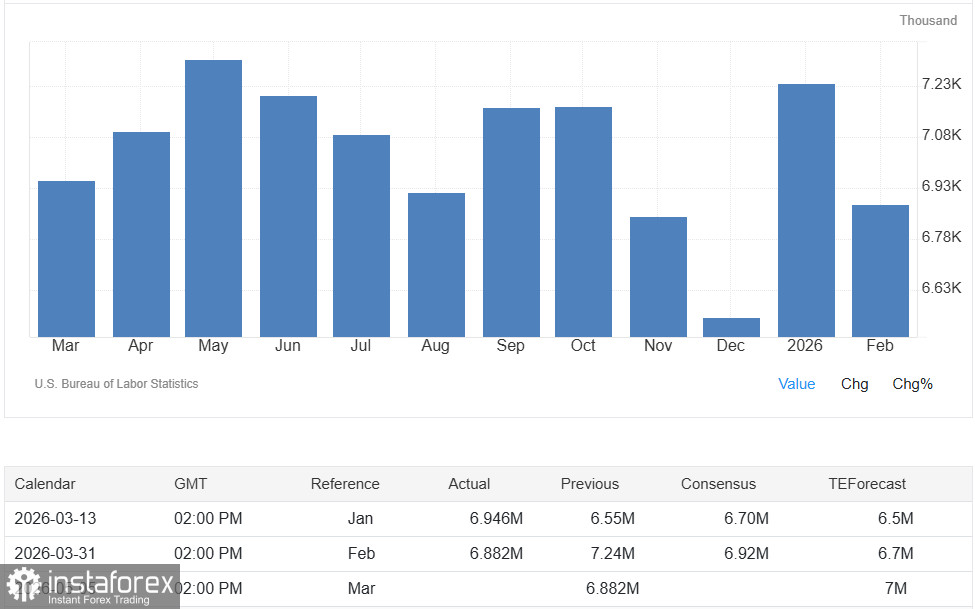

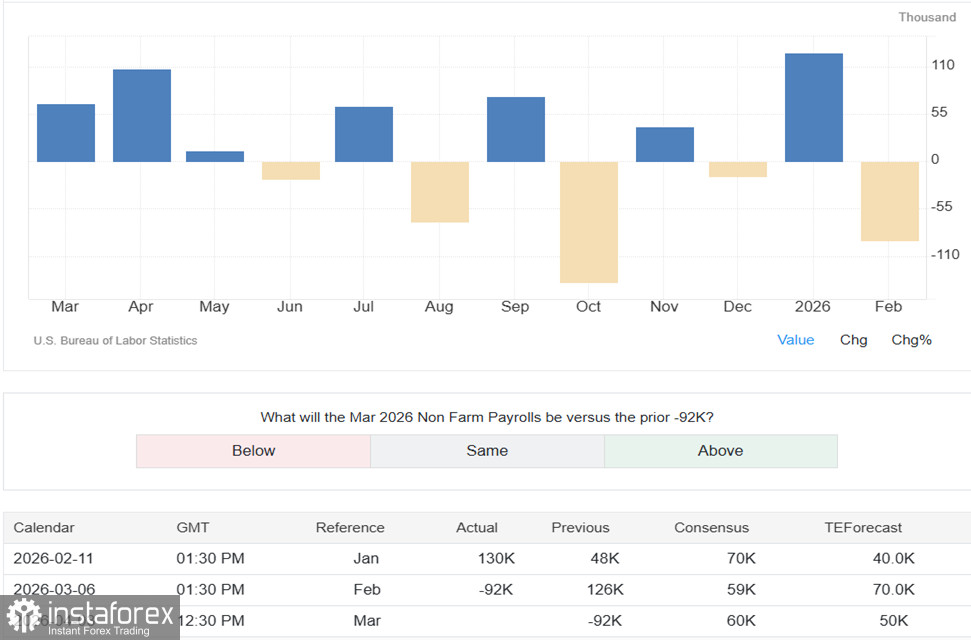

On Tuesday, JOLTS data for February were published, showing a decline in job openings in the US to 6.882 million (below the forecast of 6.920 million), and hiring fell to a five-year low of 3.1%.

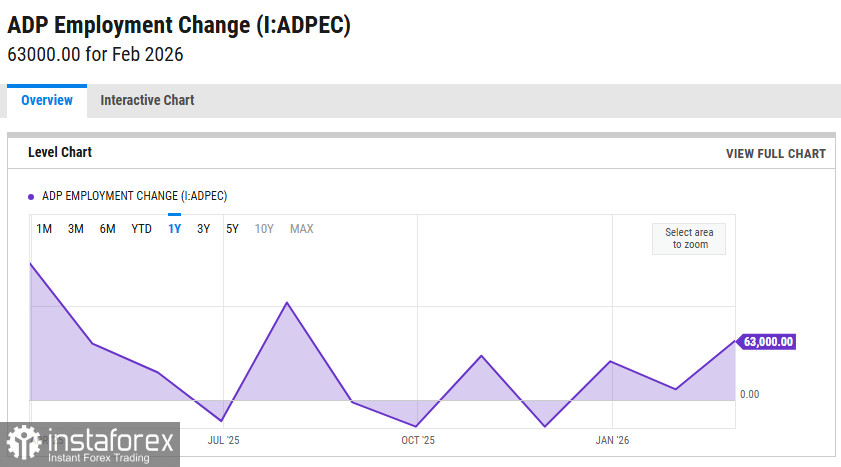

Today, ADP private payrolls for March (forecast: +40,000) and the ISM Manufacturing PMI (forecast: 52.5) are expected.

The main event of the week will be the March employment report, nonfarm payrolls, on Friday. Economists expect the creation of 60,000 new jobs after a decline of 92,000 in February, with unemployment remaining at 4.4%.

US equity markets will be closed on Friday for Good Friday, so the first reaction to the nonfarm payrolls data will appear in bond yields, the dollar, and commodity futures.

Conclusion

GBP/USD is experiencing a confident rebound amid growing hopes for de-escalation of the Middle East conflict. President Trump's comments about the possibility of ending the operation within two to three weeks and Iran's readiness for peace created a positive impulse that weakened the dollar as a safe-haven asset.

However, fundamental weakness in the British economy remains a limiting factor. UK GDP in Q4 rose by only 1.0% year on year, and experts expect further deterioration under the influence of the crisis. Prospects for Bank of England monetary policy remain uncertain: markets differ between expectations of rate increases and a continued wait-and-see approach.

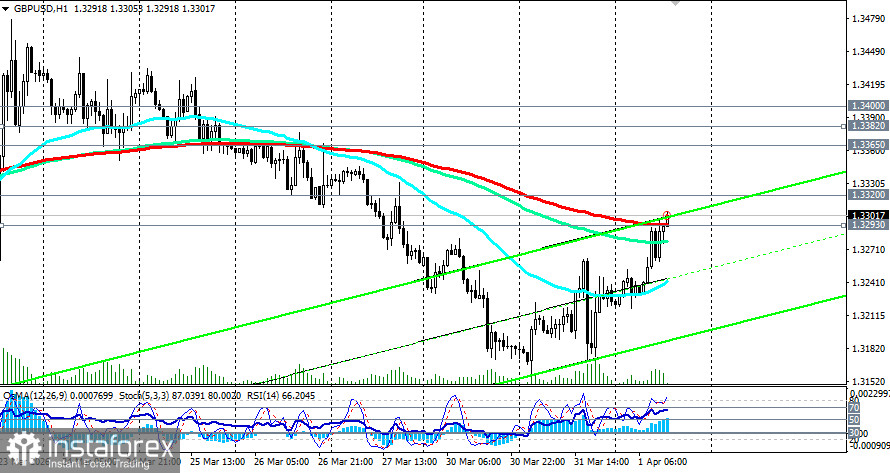

The zone 1.3278 (EMA144 on the 1-hour chart)–1.3320 (EMA50 on the weekly chart) will be the arena of a decisive battle in the coming days. Holding above it will keep the chance of testing 1.3365 (EMA200 on the daily chart)–1.3382 (EMA200 on the 4-hour chart), while a break below will open the way to 1.3260–1.3200.

Under any scenario, volatility will remain high. Investors should closely monitor developments in diplomatic contacts around the Strait of Hormuz and, most importantly, the US employment data due on Friday. As the US Secretary of Defense noted, the door for a deal is open, but in the currency market, success will favor those who can assess the balance between hopes for peace and the real inflationary consequences of a protracted conflict.